No-Doc Mortgage Loans and Self-Employed Home Loans: A Path to Homeownership

Oct 11, 2023 By Susan Kelly

When buying a home, there are a few hurdles before you can call that cozy place your own. One significant hurdle is securing a mortgage. Traditional mortgage applications can be daunting, especially for self-employed individuals or those with unconventional income sources. However, there's good news on the horizon: No-Doc Mortgage Loans and Self-Employed Home Loans.

In this article, we'll break down these mortgage options, how they work, and why they might be the key to your homeownership dreams.

What Are No-Doc Mortgage Loans?

No-Doc Mortgage Loans - It might sound like a mysterious term, but it's quite simple. "No-Doc" stands for "no documentation," these loans cater to individuals who might not have the typical financial paperwork readily available. Think of it as a simplified path to getting a mortgage.

How Do No-Doc Mortgage Loans Work?

Traditional mortgage applications require documents, including tax returns, pay stubs, and W-2s, to prove your income and financial stability. On the other hand, no-Doc Mortgage Loans require minimal documentation or sometimes none. Instead of providing extensive paperwork, you typically provide:

- A credit score: Lenders will assess your creditworthiness.

- Bank statements: Showing your income and savings.

- A down payment: The amount varies but is usually higher than traditional mortgages.

- A completed loan application: Providing information about your finances and the property you want to buy.

These loans are designed for borrowers with unconventional income sources, such as the self-employed or those with irregular income streams. If you're a freelancer, a contractor, a small business owner, or have income from investments, a No-Doc Mortgage Loan might be your ticket to homeownership.

Benefits of No-Doc Mortgage Loans

Hop on below to learn about the notable benefits of No-Doc Mortgage Loans!

- Less paperwork means less hassle.

- The approval process is often faster.

- Ideal for those with variable income.

- You can keep sensitive financial details confidential.

- Easier for self-employed individuals.

Self-Employed Home Loans: A Closer Look

Now, let's dive into another niche of home financing – Self-Employed Home Loans. These loans are tailored specifically for individuals who are their bosses. Whether you run a successful business, freelance, or work as an independent contractor, these loans cater to your unique financial situation.

How Self-Employed Home Loans Work?

The biggest challenge for self-employed individuals when applying for a mortgage is often providing a stable income. Traditional lenders may hesitate due to inconsistent earnings or a lack of traditional pay stubs. Self-Employed Home Loans offer a solution.

Instead of relying on traditional income documentation, these loans use alternative methods to evaluate your financial stability. Here's how they work:

- Bank Statements: You may need to provide several months' bank statements to demonstrate your income flow.

- Profit and Loss Statements: Your business financials, including profit and loss statements, will be scrutinized.

- Credit Score: A good credit score is still essential to secure a loan.

- Tax Returns: While not as extensive as traditional mortgages, some lenders may request recent tax returns.

Benefits of Self-Employed Home Loans

- These loans consider your real income, even if it's not consistent month-to-month.

- Tailored to the unique financial situations of self-employed individuals.

- Depending on your income, you might qualify for larger loans.

- Opens doors to homeownership for those who wouldn't qualify for traditional mortgages.

Are These Loans Right for You?

Now that you understand the basics of No-Doc Mortgage Loans and Self-Employed Home Loans, you might wonder if they fit your homeownership journey. Let's explore some factors to consider:

Your Financial Situation

Evaluate your income stability. If you have a consistent, verifiable income, a traditional mortgage might be more favorable in terms of interest rates and down payment requirements. However, if your income is irregular or you're self-employed, the flexibility of these alternative loans can be a game-changer.

Down Payment

Both No-Doc Mortgage Loans and Self-Employed Home Loans often require a higher down payment compared to traditional mortgages. Ensure you have the necessary funds available or are willing to make a substantial down payment to secure the loan.

Credit Score

Maintaining a good credit score is essential for any type of mortgage loan. Ensure your credit score is in good shape to increase your chances of approval and secure better terms.

Property Type

Consider the type of property you want to buy. Some lenders may have restrictions on the property type or location when offering these alternative loans.

Long-Term vs. Short-Term Goals

Think about your long-term goals. Are you looking for a home for many years, or is this a short-term investment? Your goals can influence which loan option is best for you.

The Application Process

Applying for No-Doc Mortgage Loans or Self-Employed Home Loans is relatively straightforward. Here's a simplified overview of the process:

Research Lenders: Find lenders who offer these loans and compare their terms and interest rates.

Gather Documentation: Collect the necessary documents, including bank statements, credit reports, and tax returns.

Submit Application: Complete the loan application, providing all required information.

Underwriting: The lender reviews your application and assesses your creditworthiness.

Approval: Once approved, you can move forward with purchasing your home.

Closing: Finalize the loan, sign the paperwork, and take ownership of your new home.

Wrapping It Up!

No-Doc Mortgage Loans and Self-Employed Home Loans are valuable tools to help individuals with unconventional income sources achieve their homeownership dreams. These loans offer a simplified application process, increased flexibility, and the potential to own a home even if you're self-employed.

Before diving in, assess your financial situation, credit score, and long-term goals. Ensure you're comfortable with the higher down payment requirements associated with these loans. By carefully considering your unique circumstances, you can make an informed decision and take that important step toward owning your own home.

-

Banking Oct 15, 2023

Banking Oct 15, 2023Credit Cards That Offer Cell Phone Protection for Loss and Damage

Discover how credit cards can protect your cell phone from loss or damage. Learn about the benefits and top credit card options providing this valuable feature.

-

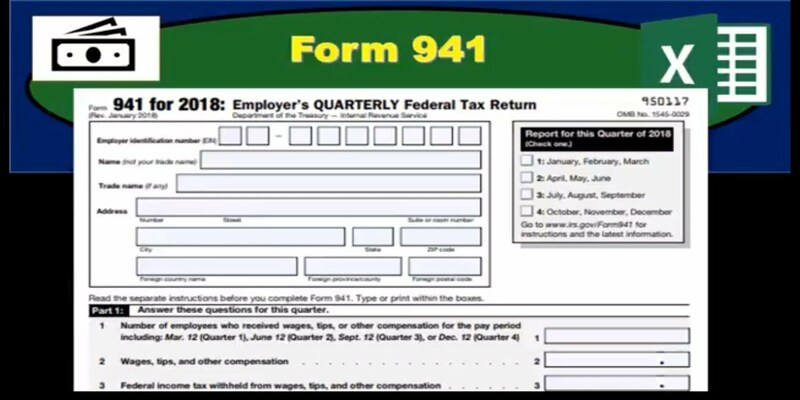

Taxes Jan 27, 2024

Taxes Jan 27, 2024What You Need To Know About IRS Form 941

A crucial tax form for businesses is IRS Form 941, the Employer's Quarterly Tax Form. Most U.S. employers are obliged to submit quarterly federal tax returns, except for individuals who only do so once a year. Businesses with employees are required to submit federal withholdings from employees on Form 941.

-

Taxes Oct 11, 2023

Taxes Oct 11, 2023Cracking the Code: Dealing with the Six Most Frequent Tax Issues in the Gig Economy

Explore the tax challenges faced by freelancers and gig workers. Discover the top six issues you need to be aware of.

-

Investment Dec 22, 2023

Investment Dec 22, 2023What Are Liquid Assets? Exploring Role and Impact in Financial Health

Discover the definition and meaning of liquid assets and why they are important when planning personal finances. Learn more