Discuss About the Debt Validation Letter and Its Importance

Oct 05, 2023 By Triston Martin

What Is a Debt Validation Letter?

When approaching you about the money you might owe, debt collectors are required by law to provide you with the following information in a debt validation letter:

- The name of the putative debtor in this situation is

- Your unpaid balance

- After the debt collector contacts you for the first time, you have 30 days to dispute the debt; after that, the debt will be treated as valid.

- If debt collectors contact you over the phone, ask for written communication instead.

- Within five days, they must mail you a debt validation letter outlining the information above.

Debt Validation vs. Debt Verification: What's the Difference?

Your debt will be validated in writing by the debt collector, who will also outline to who you owe the money and what procedures will be taken to collect it. You can write and mail a debt verification letter disputing the charge if you don't think you owe the amount (or don't think you owe as much as the collector says). You should send this letter by certified mail with a return receipt requested for added security.

Write A Debt Verification Letter

Verification letters are required in two situations:

- When interacting with a tenacious debt collector: A debt verification letter may dissuade a debt collector from making additional collection efforts if they don't have enough information. If you intend to make good on your debt: You might need further information before settling the account to ensure you're paying the right debt collector.

- According to the debt collector: If you are uncertain whether you are responsible for the debt, get in touch with the original creditor and request documentation, such as a copy of the original contract. The total sum due and the length of time it has been past due: Ask about the most recent billing statement the original creditor provided, the total amount owed at the time the debt was purchased by the collector, the time of the last payment, and whether the statute of limitations has passed. Possessing the authority to pursue debt recovery: Check to see if the debt collection company is permitted to do business in your state.

A List Of Your Rights

- You have the right to protest the debt within 30 days of getting the initial notification; otherwise, it will be considered valid.

- A statement that the debt collector must stop trying to collect the debt if you dispute it in writing within 30 days and until you give them proof of your disagreement.

- A "tear-off" document that can be returned to the debt collector with instructions on how to contest the debt should also be provided.

- A pledge that the debt collector will provide the name and address of the original creditor upon request and within 30 days of receiving it (if different from the current owner of the debt).

- The CFPB's legal debt validation notification is a standard model for debt validation notices.

Validation and Verification Letter Restrictions and Advantages

Problems with debt collection aren't always simple to address, but validation and verification letters could be of assistance. If the statutory statute of limitations has passed, a debt collector may, for example, may continue to pursue payment of the debt. You cannot be forced to pay.

The outcome of the verification and validation correspondence will not have any effect on your credit score. A debt collector's efforts to collect a debt could not appear on your credit record. Whether or not it is verified, lousy debt can stay on your credit report for up to seven years. The same is true if there is a deadline for filing a lawsuit over a debt.

If the statute of limitations has already run on the owed debt, it might also be wise to do nothing. You might unintentionally confess the debt in conversation, for instance. The collection window might be restarted as a result. Most likely, the first creditor will have all the relevant records. The best solution might be a quick transaction.

Conclusion

Debt collectors must send you a debt validation letter within five days of their initial contact if they haven't previously done so over the phone. A debt validation letter should contain the creditor's name, the amount owed, and procedures for challenging the debt.

-

Taxes Oct 01, 2023

Taxes Oct 01, 2023Bonus Tax Refund From the IRS

You would be in luck if you submitted your tax return for either 2019 or 2020 later than expected. Approximately 1.6 million persons will be refunded for previously paid fines.

-

Taxes Jan 27, 2024

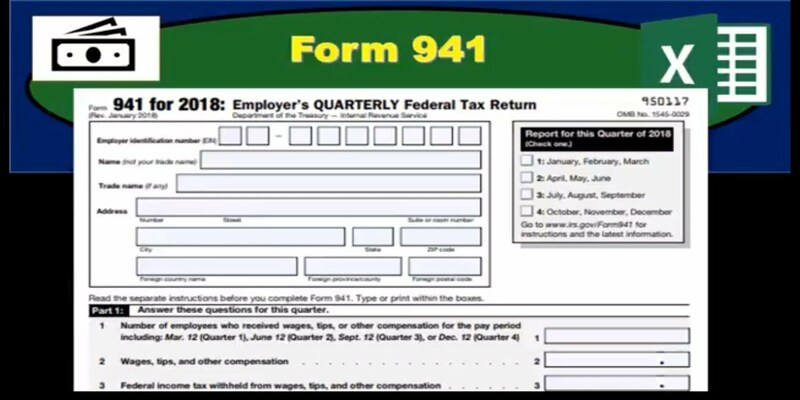

Taxes Jan 27, 2024What You Need To Know About IRS Form 941

A crucial tax form for businesses is IRS Form 941, the Employer's Quarterly Tax Form. Most U.S. employers are obliged to submit quarterly federal tax returns, except for individuals who only do so once a year. Businesses with employees are required to submit federal withholdings from employees on Form 941.

-

Investment Dec 23, 2023

Investment Dec 23, 2023Understanding Portfolio Beta

The Beta Formula is a crucial tool for investors to calculate the volatility of a stock in relation to the overall market. It's determined by comparing a stock's returns to a benchmark index such as the S and P 500. The Beta Formula helps decode how much a stock's price is likely to fluctuate compared to the market. A Beta of 1.0 signals that a stock's volatility matches the market, while a higher Beta indicates more volatility, and a lower Beta points to less.

-

Investment Nov 30, 2023

Investment Nov 30, 2023Ways to Form A Homeowners' Association

Homeowner's associations, often known as HOAs, are responsible for managing problems affecting the whole community.