Is There A Risk That Inflation May Eat Away At Corporate Profits?

Nov 01, 2023 By Triston Martin

In a nutshell, this is our point of view: while top-line sales climb, fixed expenses will assist in giving operational leverage, which will help safeguard profit margins. You may be wondering, though, what happens with the variable expenses. That is where the ability to set prices comes into play; businesses that can pass on those increased expenses to customers don't have to be as concerned about the situation. Because of this, we believe that for investors, buying stocks selectively will be more crucial than ever this year; you need to sort the wheat from the chaff.

An illustration by way of example. Consider a firm that has revenue of $100, variable expenses of $40, fixed costs of $30 (think of the cost of rent), and a profit of $30. This company would be profitable. The final margin is thirty percent.

There is no change to the fixed expenses; however, the variable costs have increased to $44 (because of the higher price of timber). We're assuming 10% annual inflation. The fixed expenses are consistent monthly (much like a rent payment). Meanwhile, this firm can pass on growing prices to customers, which results in a 10% rise in revenue, bringing the total to $110. What is there to be? A profit of $36 – a rise from the previous amount! Because the combined average of the expenses did not rise at the same rate as the sales, the profit margin has increased to about 33%.

When there is a high level of demand in the market, businesses can experience an increase in their bottom-line profits due to margin expansion. We won't know how things will play out until earnings data trickle in, but we're hopeful that well-managed and good-quality firms will come out on top.

Spotlight: Dissecting Inflation

In 2021, inflation was far higher than the Fed and we had anticipated it would be. Yet despite some signs of reduction in the most recent measurements, price rises are still too high from the point of view of consumers and decision-makers in the United States.

But here's the kicker: we believe that inflation has reached its maximum level, and we anticipate it will continue to fall for the remainder of this year. We anticipate that the core measure, which excludes fluctuations in food and energy costs, will be running about 3% year-over-year by the end of the fourth quarter (down from more than 5% in the first quarter of this year). The danger, in our opinion, is that the Fed will pursue an overly aggressive policy supporting this objective, which might lead to an unexpectedly sharp deceleration in economic growth and push the country into a recession. To better grasp this topic, it is helpful to divide the discussion into three primary categories: the housing market, the difference between commodities and services, and the labor market.

Current Evidence Suggests That A Wage-Price Spiral Will Not Occur In The Labor Market

One of the biggest macro dangers at the beginning of this year was a wage-price spiral, similar to what happened in the 1970s. In the second half of 2021, it did not seem like there would be a recovery in the labor supply. Serious labor shortages appeared in various industries, including healthcare, leisure, and hospitality. Wages were swiftly increasing at a rapid speed as firms raised compensation to get people back into the labor field. Before the pandemic, salaries increased by around 3.5% annually, which climbed to over 5.5% in the second half of 2021.

The labor market is, without a doubt, in a tight state; nonetheless, the dangers of a wage-price spiral seem to be decreasing. The percentage of working-age people participating in the labor market has significantly increased. While it is not yet established as a pattern, pay growth exhibits beginning symptoms of slowing down. More people working means there is less competition for jobs, which means there is less of a premium placed on finding qualified workers and paying them more.

It is noteworthy that broad wage growth has slowed from 5.5% to 4.3% over the last year, and the fact that economic growth is slowing due to fiscal tightening and the global commodity price shock should ensure that this trend will continue. Already, there is evidence to indicate that the economy of the United States is capable of achieving a more favorable and less inflationary equilibrium between the demand for and supply of labor.

-

Investment Nov 01, 2023

Investment Nov 01, 2023Is There A Risk That Inflation May Eat Away At Corporate Profits?

This week marks the beginning of earnings season for the fourth quarter, and there is a lot of speculation on the extent to which increased input costs will be offset by greater revenues and the amount of profit left over for shareholders.

-

Investment Nov 29, 2023

Investment Nov 29, 2023How to invest while saving for a home?

Those who are trying to save money for a down payment on a home understandably avoid making extravagant expenditures like expensive holidays or new wardrobes. But keep an eye on the details as well. These days, a bar tab for a sophisticated cocktail might set you back $16

-

Banking Oct 15, 2023

Banking Oct 15, 2023Credit Cards That Offer Cell Phone Protection for Loss and Damage

Discover how credit cards can protect your cell phone from loss or damage. Learn about the benefits and top credit card options providing this valuable feature.

-

Investment Jan 17, 2024

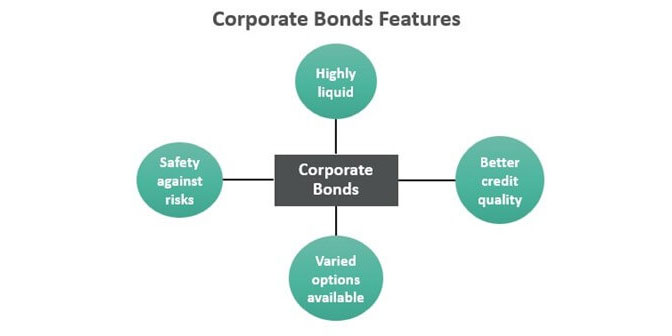

Investment Jan 17, 2024Learn: In What Ways Are Corporate Bonds Used?

A bond, a kind of debt obligation, is also referred to as an Iou. The issuing company receives financing from bond buyers. In return, the business guarantees in writing that it will pay the bond's interest and, in most cases, principal when it matures.